Canada’s credit card market offers diverse options tailored to different lifestyles—especially for travelers seeking to turn everyday spending into travel perks, cash back, and savings. Whether you’re a frequent flyer, a budget-conscious student, or an everyday spender, the right credit card can elevate your financial habits and travel experiences.

How to Choose the Best Credit Card in Canada

These top picks are credible and tailored to Canadian travelers—consider them when finding your perfect fit.

- Annual Fees: Do benefits justify the cost?

- Welcome Bonuses: Ease of earning and value upfront.

- Rewards Rates: Earnings per dollar, especially for travel-related spending.

- Interest Rates: Important for those carrying a balance (pay in full when possible).

- Travel Perks: Lounge access, no foreign fees, and travel-friendly partnerships.

- Insurance Coverage: Travel, purchase, and rental car insurance for travelers.

- Redemption Flexibility: Easy use of points for travel (e.g., Trip.com), cash back, etc.

Top 5 Credit Cards in Canada for Travel and Cashback

Here are 5 top cards covering key categories—each includes all essential details:

1. American Express Cobalt® Card (Best Overall)

Issuer: American ExpressAnnual Fee: Monthly fee (annual fee applies)

Key Benefits: Generous points on dining/food delivery, streaming, gas/transit, and 1:1 airline transfers.

Best For: Most Canadians, casual travelers, frequent diners.

2. Scotiabank Gold American Express® Card (Top Travel Rewards)

Issuer: Scotiabank

Annual Fee: Annual fee (waived first year)

Key Benefits: Generous Scene+ points bonus; elevated points on groceries and dining; no foreign fees, travel insurance.

Best For: Travelers who spend on groceries/dining.

3. CIBC Dividend Visa Infinite (Top Cashback)

Issuer: CIBC

Annual Fee: Annual fee (waived first year)

Key Benefits: Enhanced cash back in the first few months; elevated cash back on groceries/bills and gas/transit.

Best For: Cashback lovers, everyday spenders.

4. Rogers Red World Elite Mastercard (Top No-Fee Cashback)

Issuer: Rogers Bank

Annual Fee: $0

Key Benefits: Consistent cash back (higher for Rogers customers); no foreign fees, basic travel insurance.Best For: Budget travelers, Rogers customers.

5. BMO Cashback® Mastercard®* for Students (Top Student Card)

Issuer: BMO

Annual Fee: $0

Key Benefits: Enhanced cash back in the first few months; elevated cash back on groceries and bills; easy student approval.

Best For: Students building credit.

582646 booked

582646 booked

Best Credit Cards in Canada Compared: Side-by-Side Overview

Quick reference: side-by-side comparison of our top 5 picks:

Card Name | Annual Fee | Rewards Rate | Best For | Quick Verdict |

|---|---|---|---|---|

American Express Cobalt® Card | Annual fee (monthly option) | Elevated points on dining, streaming, gas/transit; standard on all else | Most Canadians, casual travelers | Best overall—flexible rewards for everyday use |

Scotiabank Gold American Express® Card | Annual fee (waived first year) | Elevated points on groceries, dining, gas/transit/streaming | Travelers, grocery spenders | Top travel rewards with great everyday points |

CIBC Dividend Visa Infinite | Annual fee (waived first year) | Elevated cash back on groceries/bills, gas/transit; standard on all else | Cashback lovers, everyday spenders | Top tiered cashback with travel insurance |

Rogers Red World Elite Mastercard | $0 | Consistent cash back (higher for Rogers customers) | Budget travelers, Rogers customers | Best no-fee cashback with no foreign fees |

BMO Cashback® Mastercard®* for Students | $0 | Elevated cash back on groceries, bills; standard on all else | Students | Best student card for credit building and cashback |

Maximizing Your Credit Card Rewards When Travelling in Canada and Abroad

Maximize travel rewards with these simple tips:

- Match cards to categories: Use travel cards for dining, cashback cards for gas to earn more.

- Avoid foreign fees: Use cards like Scotiabank Passport or Rogers Red to save 2.5% on Trip.com and abroad.

- Use built-in insurance: Book trips with your card to activate travel insurance—no extra cost.

- Time applications: Apply before big Trip.com bookings to hit welcome bonus thresholds.

- Redeem for travel: Points are more valuable for Trip.com bookings than cash back.

Using Travel Credit Cards for International Bookings

Use Canadian travel cards for international bookings with these tips:

- Foreign fees: Waived on Scotiabank Gold/Passport cards—save on Trip.com international bookings.

- Insurance activation: Book trips with your card to unlock travel insurance (check terms).

- Redeem points: Use points for international flights/hotels via rewards portals or Trip.com.

- Currency conversion: Pay in local currency to avoid merchant fees.

Tips for Meeting Welcome Bonus Spending Requirements

Meet welcome bonus thresholds responsibly with these tips:

- Time applications: Apply before big expenses (Trip.com bookings, groceries).

- Pre-pay bills: Use the card to pre-pay phone/internet bills to hit thresholds.

- Use for daily spending: Put groceries, gas, and dining on the card (pay in full).

- Split purchases: Divide big buys between cards (only if you can pay in full).

Never overspend for bonuses—skip if you can’t meet thresholds with regular spending.

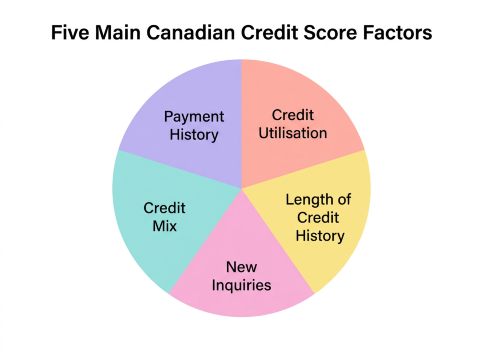

What Affects Your Credit Score in Canada? Key Factors to Know

Your credit score impacts loans, rentals, and cards—key factors (including the biggest “killer”):

- Payment History (35%): Missed/late payments are the biggest killer—pay on time, even the minimum.

- Credit Utilization (30%): Keep below 30% (10% ideal) of your credit limit.

- Credit Age (15%): Keep old cards open to lengthen your credit history.

- Hard Inquiries (10%): Each card application lowers your score slightly—space out applications.

- Account Diversity (10%): A mix of credit types (cards, loans) helps—no need for extra debt.

The biggest credit score killer: missed/late payments. Set up auto-pay to avoid this.

Credit Utilization: The Most Impactful Factor (After Payment History)

Credit utilisation = (balance ÷ credit limit) × 100%. Keep it below 30%—lenders see high utilisation as risky.

Why does it matter? Lenders see high utilisation as a sign that you’re relying too much on credit, which makes you a riskier borrower. Keeping your utilisation below 30% is key to maintaining a good score—aim for 10% if you can.

Pro tip: A new card can lower utilisation (more credit limit, same balance)—don’t overspend!

How Applying for Multiple Credit Cards Affects Your Score

Multiple card applications can hurt your score—here’s what to know:

- Hard Inquiries: Each lowers your score slightly, fades after several months, stays for a couple of years.

- Credit Age: New cards shorten average age—impact is small and temporary.

- Strategic Applications: Space out applications by several months—apply only for useful cards.

A few cards per year is fine—too many in a short period hurts your score. Choose cards that fit your lifestyle.

Final Verdict: Which Is the Best Credit Card in Canada for You?

Choose your card based on lifestyle—here’s how:

- Frequent traveler: Scotiabank Gold (everyday points) or Passport (no foreign fees). Redeem on Trip.com.

- Cash back lover: CIBC Dividend (tiered) or SimplyCash (flat-rate, no fee).

- Budget/student: Rogers Red (no fee, cash back) or BMO Student Card (no fee, easy approval).

- Balance carrier: MBNA True Line (low interest, no fee).

- Most Canadians: American Express Cobalt (flexible, everyday rewards).

Use your card responsibly: pay in full monthly, keep utilisation low, and choose a card that fits your spending. Turn everyday buys into travel or cash—happy spending!

Earn Trip Coins & Membership Cashback

Before swiping your card, do grab these instant savings with Trip.com’s Membership Program. Earn Trip Coins by booking travel, writing reviews, or sharing trip moments. These coins act like cashback:

- 100 Trip Coins ≈ CAD 1.37 on hotels, flights, attractions, and more.

- No minimum redemption—use them even for small discounts!

- Stack Trip Coins with promo codes during campaigns for double the savings.

Pro Tip: Leave a review after your trip—it’s an easy way to earn extra Trip Coins for future bookings.

Credit Card vs Other Payment methods

Trip.com supports global and local payment methods such as:

- Credit/Debit Cards: Visa, Mastercard, Amex, UnionPay, and more.

- Digital Wallets: PayPal, Apple Pay (iOS), Google Pay (Android/Web).

- Trip Coins & Gift Cards: Offset costs instantly with earned coins or prepaid gift cards.

Payment Method | Pros | Cons |

|---|---|---|

Credit Cards | Earn rewards, travel insurance, $0 fraud liability | Time needed to input card details |

PayPal | No card details shared | No rewards unless linked to a rewards card |

Digital Wallets (Apple/Google Pay) | Fast checkout | Rewards depend on linked card’s terms |

Trip Coins | Instant discounts on bookings | Limited to Trip.com ecosystem |

Digital Wallets (Apple/Google Pay) | Fast checkout | Rewards depend on linked card’s terms |

Download the App for App-Only Discounts

Download the Trip.com app now and unlock exclusive app-only discounts! These app-only deals can stack with flash sales to deliver substantial savings on fares departing Canada. Use the QR code to get instant savings on flights and hotels, available for both Android and Apple users.

[10% OFF] Global Hotel Recommendations

FAQ: Best Credit Cards for Miles & Cashback

-

What is the best overall credit card to have in Canada?

-

What is the biggest killer of credit scores in Canada?

-

How many credit cards should I have in Canada?